How Much Coverage Is Enough?

Determining the right amount of insurance is one of the trickiest problems in personal financial planning. Rather than picking a number based on affordability or a generic rule of thumb, coverage should be tied to a person’s age, income, financial responsibilities, and long-term goals — all of which shift over time. Insurance is therefore not a one-time purchase but a tool that needs to be revisited at every stage of life.

Understanding Human Life Value

The core purpose of life insurance is to replace income. Financial planners use the idea of “human life value” — the present value of everything a person is expected to earn over their working life — as the benchmark for how much protection is needed. The goal is to make sure dependents are not left financially exposed if the earner dies unexpectedly.

Starting Your Career

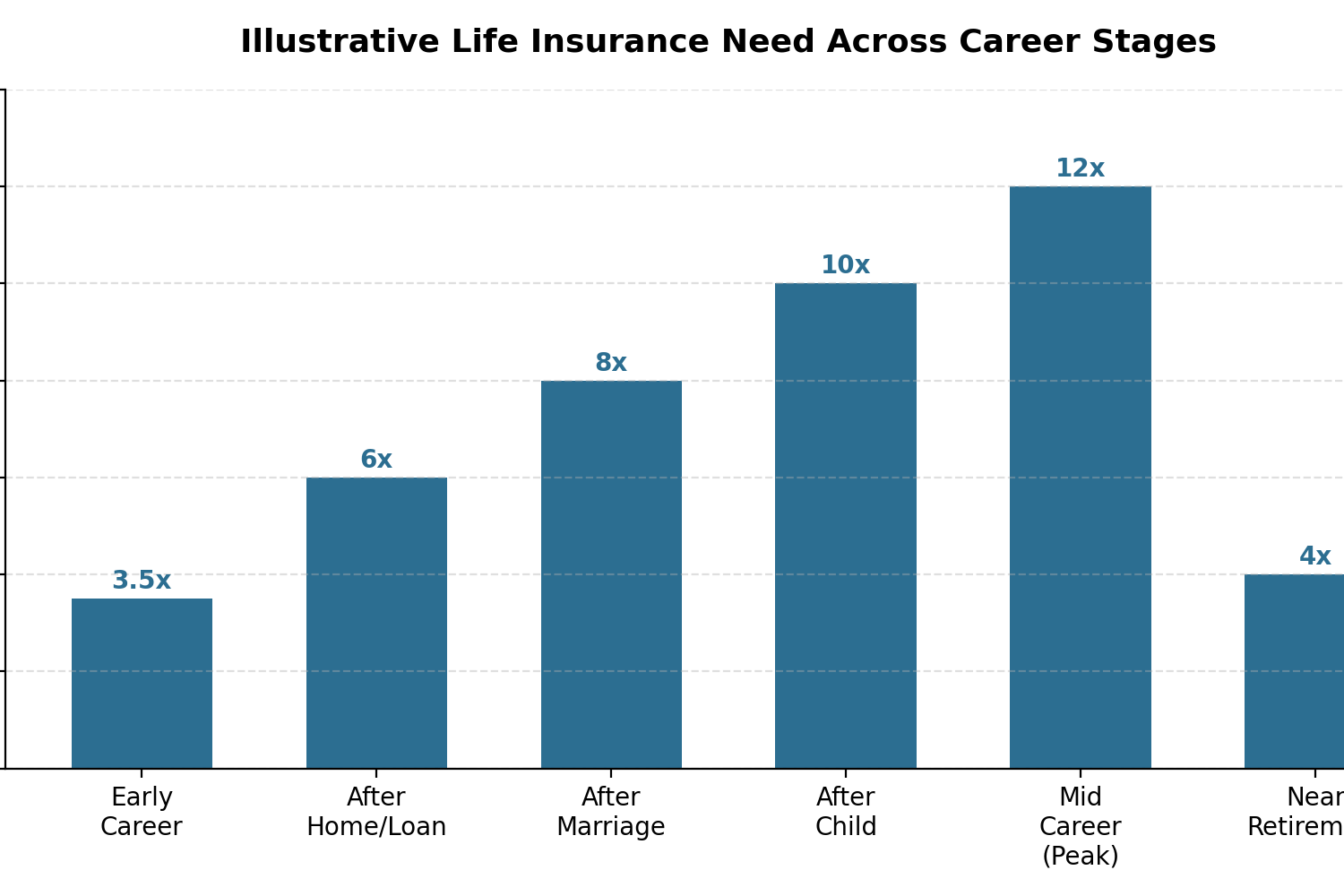

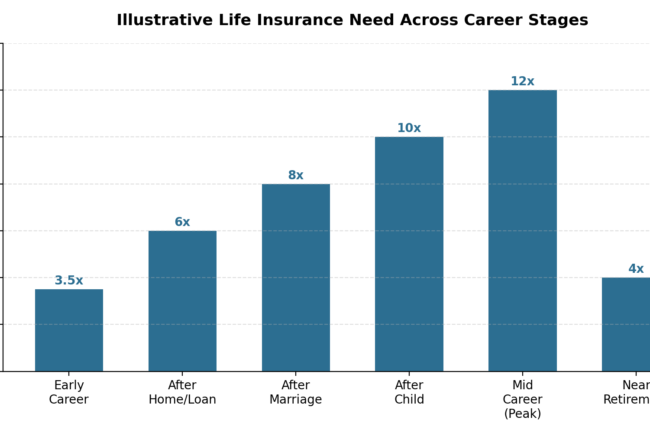

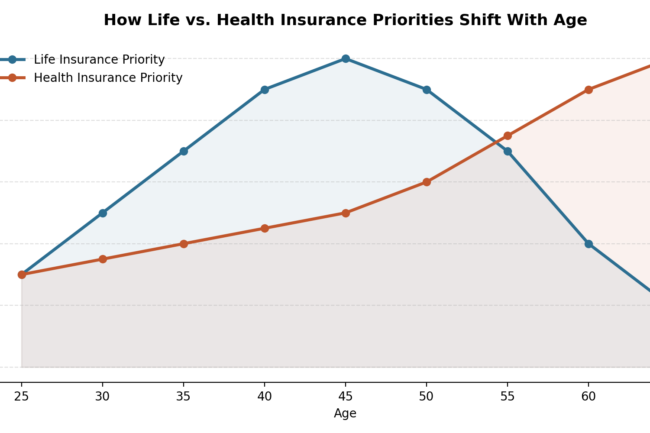

At the start of a career, needs are modest: fewer dependents and fewer liabilities mean coverage of roughly three to four times annual income is often enough to look after parents, settle small debts, and build a cushion. Health insurance, though, matters from day one, since medical costs can erode savings even for someone just starting out.

Illustrative life insurance coverage as a multiple of annual income, by career stage.

Growing Responsibilities

As careers progress, income rises but so do commitments — homes, cars, education loans. These liabilities push up the required coverage, because a good insurance plan should clear outstanding debt so it does not fall on the family. Big purchases or new loans should trigger a fresh look at coverage.

Planning for the Future

Marriage is a turning point: planning shifts from protecting one person to protecting a household. Coverage should now reflect the family’s spending, future lifestyle needs, and what the surviving spouse would require to stay financially independent.

Having children raises the stakes further. Parents take on decades of future costs — schooling, healthcare, and eventually the child’s transition into adulthood — all of which need to be funded even if the parent is not there to earn. Insurance at this stage is not just about replacing salary; it is about keeping the family’s long-term goals on track.

Education costs deserve special attention because they tend to rise faster than general inflation. A coverage amount that looks sufficient today can fall short fifteen or twenty years later if this is ignored, so plans need periodic revision to keep pace with the real, inflated cost of schooling.

Mid-Career Review

Mid-career is usually the busiest phase for financial obligations — ageing parents, home loans, children’s education, and retirement savings can all be running at once. This calls for the most thorough review of insurance, ideally aligned with the overall financial plan, and updated whenever income, family circumstances, or business situations change.

Retirement Priorities

By retirement, life insurance needs typically shrink because debts are paid off and children are self-sufficient — fewer people depend on the retiree’s income. Health insurance, however, becomes far more important, since medical costs rise with age and can quickly erode savings built up over a lifetime without solid coverage.

Two more principles run through the whole picture. First, inflation steadily erodes the value of a policy bought years earlier, so coverage needs periodic top-ups. Second, personal circumstances matter: people with substantial assets or investments may need less life insurance, while the self-employed or those with irregular income — who lack employer benefits — usually need more.

The essay’s overall message: there is no fixed “right” amount of insurance. It is a moving target shaped by income replacement, human life value, debt, inflation, and life’s milestones, and it needs regular review to stay adequate.